The freight recession is over. That 18-month malaise was triggered by the worldwide collapse of oil prices at the end of 2014. Energy exploration and fracking petered out, and the accompanying freight dried up. Fuel prices dropped, and carrier revenues fell due to the declining fuel surcharges. To add insult to injury, line haul rates fell, too, in a cycle of year-over-year declines that lasted through the middle of 2016.

Freight volume and rates finally began to revive in May 2016, and year-over-year volume comparisons turned positive in August. Instead of tapering off after October, as retail freight did in years past, a boom market emerged for truckload transportation in November and December. E-commerce was a major source of spot market freight for what is usually a quiet season, boosting truckload rates to a surprise peak in the last two months of the year.

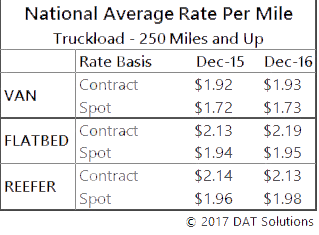

A quick look at December's average rates, with year-over-year comparisons, confirms those trends:

Dry van rates rose by a penny, the first positive year-over-year comparison in a long time. Granted, some big markets like Atlanta and Dallas remained quiet this December. Instead, rates and volumes shot up in places like Memphis and Columbus, both associated with e-commerce fulfillment, and even Denver and Seattle exhibited unusually robust rates and shipping patterns.

Refrigerated van spot rates were nearly as high in November and December, at $1.95 and $1.96 per mile, as they were at the June peak of $1.98. Contract rates for reefers actually reached June levels in December at a national average of $2.12 per mile. For flatbeds, spot rates are slightly ahead of last year's levels, and contract rates are up by a full 6¢ per mile, compared to December 2015.

So rates have recovered, but that was 2016. Why the optimism going forward?

In addition to the surge in e-commerce, the U.S. economy has the potential to become stronger in a number of ways, as the Federal government transitions to a new administration. An increase in demand for freight transportation would be one result, if these new policy proposals are implemented:

- Anticipated higher levels of infrastructure spending

- Corporate investment, with lower tax rates and repatriation of foreign earnings

- Political and economic measures that relax regulation and stimulate growth

Further, an ongoing slowdown in fleet additions by the largest carriers may lead to tighter truck capacity. By the end of 2017, electronic logging devices (ELDs) will be mandatory, and shippers are likely to require them even earlier in the year. By mid-year, carriers that still lack ELDs will find it increasingly difficult to maintain ongoing relationships with shippers, and with the large fleets and freight brokers that serve them.

This combination of political, regulatory, and economic factors should yield additional rate increases for motor carriers in 2017. Those factors will further accelerate the real momentum that has been building since the middle of 2016. That improvement has already led to declining unemployment rates, rising real wages for workers, and economic growth of almost 3% in the second half of 2016.

Oil prices are still a wild card. Can the U.S. economy grow domestic energy production without causing damage to the worldwide economy? Will a strong dollar and the prospect of renewed protectionism strangle trade? How will future tax cuts and/or infrastructure spending affect the Federal budget and its deficits? The answers to these questions remain largely unknown.

Rates in 2017

All in all, the likelihood of increased demand and reduced capacity should result in rate increases, in the low to middle single digits. Rates may go even higher if the ELD mandate removes significant truckload capacity by the third quarter of 2017. At that point, spot market freight pricing could become very interesting, as it is precisely the smallest fleets who will be the last ones to jump on the ELD bandwagon, and those small operators comprise the bulk of spot market capacity.

Advice for 2017: Plan for growth, but keep a close watch on various markets. As we have learned from the current freight season, it's not business as usual.

Note: This article was adapted from DAT’s blog post on www.DAT.com. It was first published in January, 2017.

FTS Plus+ partners with DAT to offer a special on the TruckersEdge load board to its members. Sign up for DAT TruckersEdge today and get your first 30 days free and 10% off for life by signing up at www.truckersedge.net.

*This offer is available to new TruckersEdge subscribers only.